The latest edition of the DOE report, Adoption of Light-Emitting Diodes in Common Lighting Applications, models the current state of the U.S. general-lighting market and provides analysis on realized and potential energy- and money-saving benefits associated with LED lamps and luminaires.

- Adoption of Light-Emitting Diodes in Common Lighting Applications (Report, August 2020)

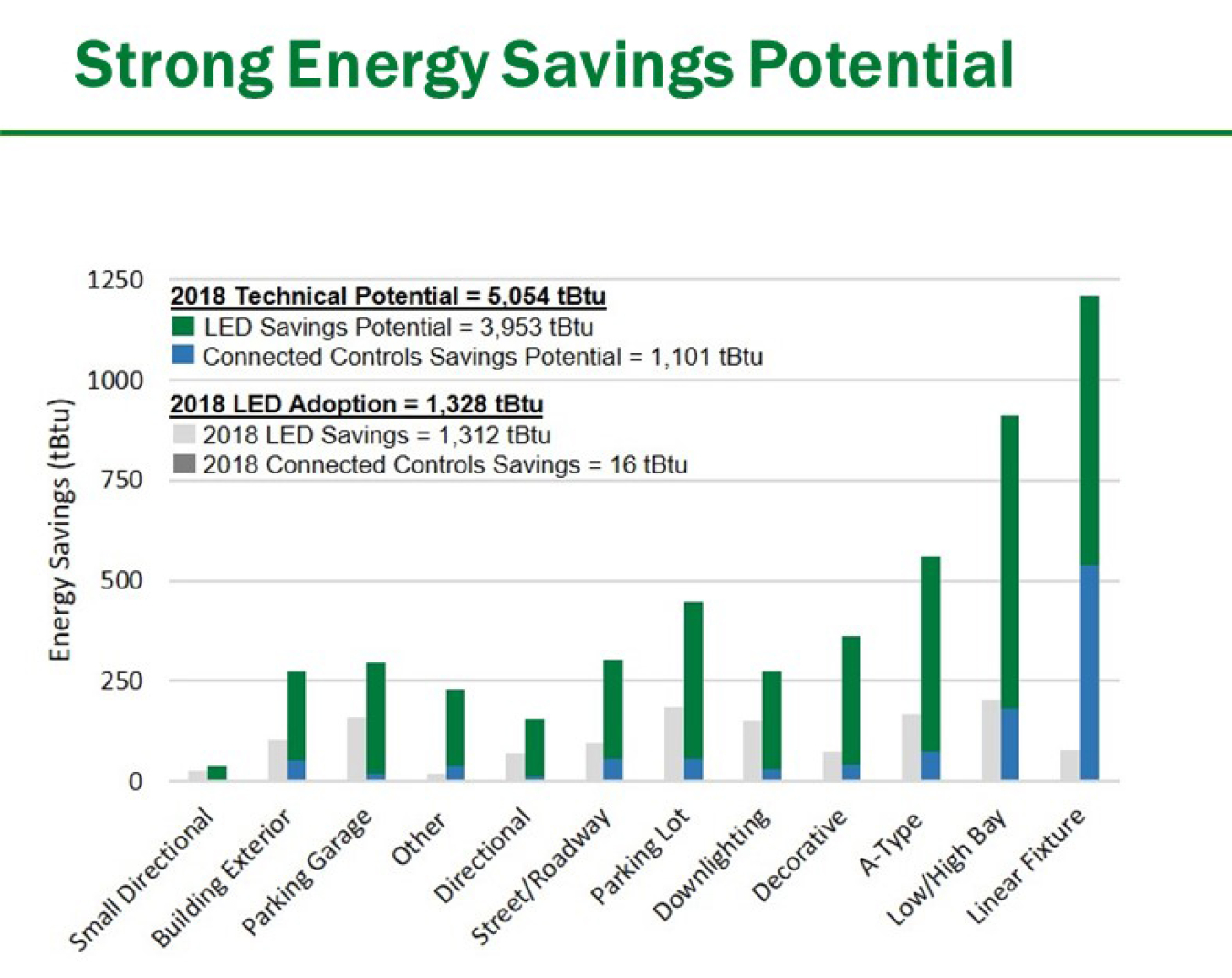

The new report estimates annual U.S. energy savings of 1.3 quadrillion Btu (quads) in 2018 due to LED adoption, equivalent to cost savings of $14.7 billion for consumers and about 5% of total electricity use from buildings in 2018. The theoretical potential for widespread use of the most efficient, connected LED products would amount to over 5 quads of energy savings, nearly four times greater than present energy savings and equivalent to about 20% of total building electricity use in 2018. Key findings of the report include:

- From 2016 to 2018, installations of LED products have increased in all applications, roughly doubling to 2,325 million units or 30.0% of all general illumination lighting.

- A-type lamps represent nearly half of all LED lighting installations and have increased to an installed penetration of 32.9% in this application. Decorative lamps have the lowest installed LED penetration presently, but nonetheless saw an increase from 7.9 to 16% from 2016 to 2018.

- The outdoor lighting market has seen greater penetration of LEDs (51.4%) than indoor lighting (29.8%), but total LED installations are considerably higher for indoor applications (2.2 billion vs. 100 million).

- Penetration of connected lighting controls remains small, with only 0.2% of lighting installed with these systems in 2018. However, the potential for connected controls to contribute to LED energy savings is substantial, estimated at 1.1 quads annually if fully implemented.

For indoor applications, low/high bay fixtures and A-type lamps have provided the greatest energy savings to date. The majority of potential savings, however, is associated with low/high bay and linear fixtures, which are staples of commercial and industrial buildings that require high light output and long operating hours. These buildings benefit most from connected capabilities, which are essential to realizing maximal lighting energy- and cost-savings.

The outdoor sector has seen greater LED adoption in nearly every application than the indoor sector, contributing 40% of the total energy savings from LED lighting in 2018. Utilizing the most efficient LEDs in all applications would amount to over a quad of annual energy savings in the outdoor sector alone, equivalent to about 9% of commercial building electricity use in 2018.

Low/high bay, parking lot and garage, and A-type LED products currently save the most energy, but linear fixtures offer the highest savings potential. Progress in control technologies will be key to unlocking the full potential energy savings.