"Savings must exceed payments." This is the cardinal rule of federal energy savings performance contracts (ESPCs). Savings must exceed payments in each contract year. Savings that may be used to pay the energy service company (ESCO) include energy and water cost savings and energy- and water-related cost savings.

Energy and water cost savings can result from reduced equipment usage or from improved efficiency. Utility costs can be decreased because of reduced peak demand, fuel substitution, renegotiated utility rates, and other factors.

Energy- and water-related cost savings are from reduced expenses for operations and maintenance (O&M) or repair and replacement (R&R) of energy-consuming systems (recurring savings). One-time energy-related savings can result from cost avoidance provided by the project. For example, the agency may have been planning to replace a chiller using funds appropriated for energy and related expenses, and then decide to include the chiller replacement in the ESPC project. The money that would have been used to replace the chiller in the absence of the ESPC project can be used to help pay for the ESPC project.

To learn more about the financial structure of an ESPC, see the Practical Guide to Savings and Payments in ESPC Task Orders.

Calculating Savings

There are two fundamental factors that drive energy savings: performance and usage.

- Performance describes how much or how little energy is used to accomplish a specific task.

- Usage describes how much of the task is required, such as the operating hours for a piece of equipment.

Examples of Calculating Savings

Lighting provides a simple example. Performance is the watts required to provide a specific amount of light. Usage is the operating hours per year.

A chiller is a more complex system. Performance is defined as kW/ton, which varies with load. Usage is defined by cooling load profile and ton-hours. In all cases, both performance and usage factors need to be known to determine savings.

Savings Uncertainty

Uncertainty in energy savings performance contracts is simply the inability to exactly and consistently quantify the savings. Unlike energy, energy savings cannot be directly measured. Instead, savings are estimated by comparing the way a system operated before and the way it operated after a measure was installed.

Even though a large number of parameters can be measured, there are still errors associated with measuring equipment. Because not every piece of equipment can be measured, sampling techniques are often used, which can introduce additional uncertainty. Random variations occur in building energy use or equipment that may be related to human behavior, weather conditions, or other factors. Simplifying assumptions is sometimes used when it is too difficult to measure or estimate a parameter, introducing additional uncertainty.

All of these factors can prevent an absolutely accurate measurement of savings. In measurement and verification (M&V), the goal is to minimize uncertainties to acceptable levels, understanding that they can never be completely eliminated or perfectly controlled. For more information about M&V, see:

- M&V activities required in the ESPC process

- M&V options for ESPCs

- Using M&V to manage risk in energy- and water-saving projects.

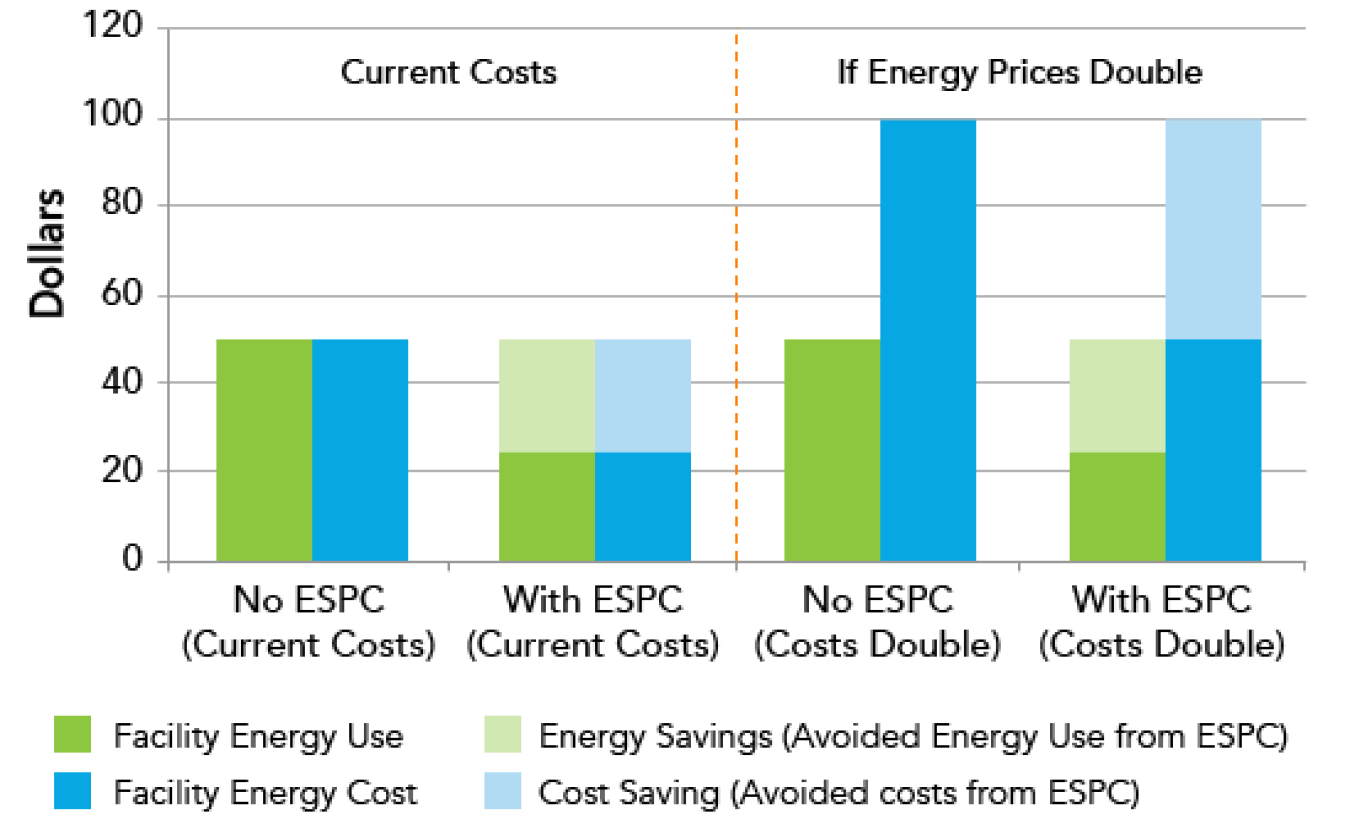

Energy Prices and Energy Savings Performance Contract Savings

The effect of energy prices on ESPC savings is a common source of confusion. When energy prices go up, savings appear to evaporate because total utility costs go up. However, ESPC savings or actual cost avoidance increases as well. The key issue is what costs would have been without the ESPC. The ESPC is in fact a hedge against higher energy prices, as total energy usage is reduced.

The chart below shows the value of an ESPC given changes in energy prices. This information can be useful for explaining to colleagues and decision makers how ESPCs save energy and money whether utility costs increase or stay the same.